.png)

One of the biggest misconceptions sellers have is that maximizing value before a sale means taking on a major renovation.

That's almost never true.

One of the first things we evaluate when walking into a new listing is not whether a seller should gut renovate, but what may distract buyers from emotionally connecting to the space and what can be done to make the apartment feel brighter, fresher, more aspirational, and easier to picture living in.

And in most cases, that is where we focus.

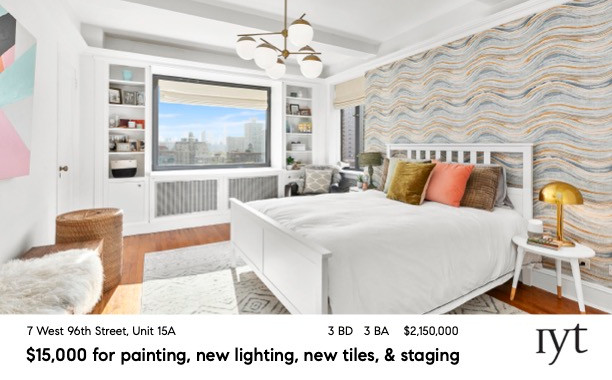

Paint is one of the clearest examples. But not just on the walls. We often recommend painting cabinetry, bathroom vanities, built-ins, or outdated trim when the existing finish feels dated, chipped, worn, or simply does not photograph well within the space. Those relatively minor changes can completely shift how an apartment feels without the cost, timeline, or disruption of a full renovation.

Lighting is another high-impact update. Replacing dated fixtures with cleaner, simpler options can make a space feel much more current almost immediately. Goodbye boob lights.

Then there are the softer details buyers may not consciously notice, but absolutely react to.

Fresh linens brighten a room and instantly elevate it, whether that means crisp bedding, updated towels, or a better shower curtain. We often switch out throw pillows for more modern patterns and textures that photograph better and make the apartment feel more current.

Plants soften rooms and make them feel cared for. Even good fake plants can have this effect.

Rugs are not just decoration.

They define spaces.

We pay close attention to scale and dimensions because the wrong rug can actually make a room feel smaller or awkwardly proportioned.

Things like coffee table books, artwork, and accessories can also help shape the overall feeling of a space, whether that vibe is more bohemian, artistic, academic, minimal, or classic.

In reality, we rarely advise sellers to take on major renovations before listing. In more than a decade of selling Manhattan and Brooklyn real estate, we have only recommended full kitchen renovations twice before listing — both in situations where we believed the increase in sale price would far exceed the actual renovation cost, which is very rare. (And we were right.)

We want buyers to respond emotionally to the apartment. They need to feel it that is has been well maintained and is easy to move into. We want them to feel connected. We want them to feel “this is how I want to live." Those feelings last past the showing. Those feelings have them up at night. Those feelings get offers.

Before or After? Do you think the costs were worth it?